Affordable Housing Op-Ed Series Part 1: Breaking Down Durham’s Barriers to Homeownership

October 15, 2025

Part 1: Breaking Down Durham’s Barriers to Homeownership

Nimasheena Burns, President and CEO, Habitat for Humanity of Durham

Despite Durham’s prosperity, too many families remain locked out of homeownership. The challenges go beyond personal budgeting or credit scores – they are systemic barriers entrenched in our housing market. In Durham County today, roughly 39,000 households (out of ~122,000) cannot afford their current housing. That means nearly one in three families is living cost-burdened, paying over 30% of income for shelter. These cost burdens hit minority communities hardest and are driving a silent crisis of displacement and distress.

One major barrier is cash, not credit. Many low-income families do qualify for 30-year fixed mortgages; their incomes and credit scores meet lending criteria. The deal-breaker is the upfront cash needed – the down payments, closing costs, and mortgage insurance. In today’s market, these upfront costs have become “the new barriers” to entry. According to the North Carolina Housing Finance Agency, Durham’s housing stock is so tight that buyers effectively need a 20% down payment to win a home – far above the typical 5% that suffices elsewhere. Nationally, the median loan-to-value for first mortgages is ~95%, reflecting that most buyers put only ~5% down. But in Durham, competition and low inventory mean cash offers and big down payments rule the day. For a $300,000 starter home, 20% is $60,000 – an insurmountable sum for working-class families. They aren’t losing out because of poor credit or irresponsible spending; they’re losing because they lack generational wealth or sizable savings. Credit readiness isn’t the issue – the lack of down payment assistance is.

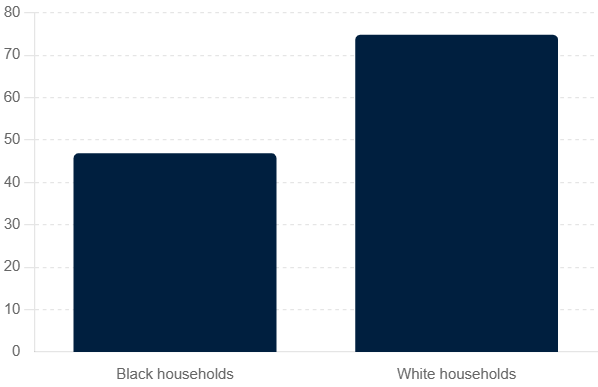

Homeownership rates in Durham County reveal a stark racial gap: only 47% of Black households own homes, compared to 75% of white households. This 28-point disparity underscores the systemic inequities in mortgage access and wealth. (Data source: NC Housing Finance Agency & Urban Institute)

Compounding this is a legacy of racial disparity in mortgage access. Durham’s homeownership rates lay this bare: only 47% of Black households own their homes, versus 75% of white households – a 28-point racial gap. This gap isn’t simply the product of individual choices; it reflects decades of discrimination, lower appraisals in communities of color, and fewer family assets to draw on for down payments. Even at equal incomes, Black borrowers on average receive smaller loans and higher interest rates, or they shy away from the process entirely after generations of redlining-induced distrust. As Habitat for Humanity of Durham’s CEO – and as a Black woman who grew up in North Carolina – I know these hurdles are not hypothetical. They are the stories I hear daily: families with stable jobs and good credit denied the chance to buy because they can’t amass a huge lump sum or because they encounter subtle biases in underwriting.

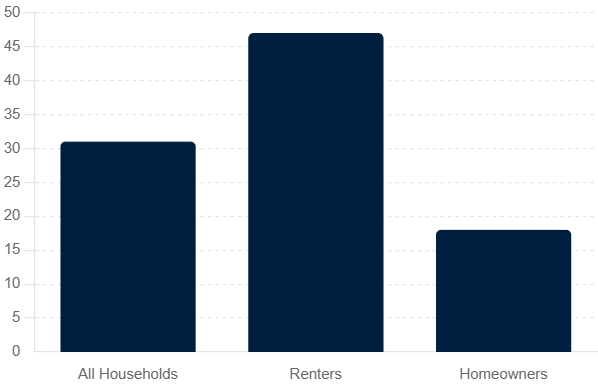

Durham’s working families are also being squeezed by rising costs and an alarming uptick in foreclosures. Over 31% of all Durham households are cost-burdened by housing. Among renters, nearly half spend over a third of income on rent, and for homeowners the figure is about 18%. When any unexpected expense or rate hike hits, these families have no wiggle room. The result? Some lose the very homes they fought so hard to attain. In Durham County, 254 families faced a foreclosure in the past year. Many of those homeowners fall in the 30%–50% of Area Median Income (AMI) range – folks who earn too much to qualify for a lot of aid, but far too little to absorb rising taxes, insurance, and adjustable mortgage rates. We’re seeing this especially in our historically Black neighborhoods: elders on fixed incomes or modest pay are getting squeezed by higher costs and are at risk of losing homes that have been in their family for generations. It’s a cruel irony that even as housing values climb, the people who most need the stability of homeownership are struggling to hang on.

What’s clear is that these barriers are not about personal failure – they are about system failure. We as a community must address the structural problems: the wealth gap, the lack of affordable starter homes, and the dearth of support for first-time buyers. Habitat for Humanity of Durham has long prepared families with financial education and sweat equity, but in 2023 we find that isn’t enough on its own. We need bold, targeted interventions to level the playing field. For example, a Down Payment Assistance (DPA) program could be transformative. Imagine a Durham County initiative providing, say, $50,000 per eligible family as a zero-interest forgivable second mortgage. That could instantly knock down the biggest wall preventing home purchase. (In fact, our neighbors in Orange County have piloted something similar, and it works.) Such a program would help not just the individual families, but unlock private mortgage capital that stays sidelined without that initial boost – a 7:1 leverage of public to private dollars by one estimate.

We also must expand housing counseling and financial literacy support. At Habitat Durham, we recently increased our required financial coaching to 15 hours of in-person training for prospective homeowners. This isn’t because our families are uneducated about money – it’s because the stakes are higher now than ever. We want our homebuyers to feel confident navigating everything from property taxes to maintenance costs. When you’re stretching every dollar to keep your home, knowledge truly is power. Empowered homeowners are far less likely to face foreclosure, even in hard times.

Finally, addressing racial inequities in homeownership means intentionally reaching out with these resources to communities of color. We partner with local churches, employers, and community groups to spread the word that owning a home in Durham is possible – and we’re here to help make it happen. The fact that nearly 3 out of 4 white families own homes in our county while barely half of Black families do is unacceptable, problematic but also fixable. By investing in down payment help, affordable home construction, and fair lending advocacy, Durham can begin closing that gap.

This Affordable Housing Month, let’s commit to tearing down the barriers to homeownership. Local policymakers must prioritize funding for down payment assistance and preserve affordable homeownership opportunities in EVERY DEVELOPMENT PLAN. Lenders and realtors must uphold equitable practices so that qualified buyers of all races are not left behind. Philanthropists and employers can join us by donating land or housing to Habitat for Humanity of Durham or even invest in their own employer-assisted housing programs. Local elected officials can continue to develop the Revolving Housing Trust Fund and expand Down Payment Assistance programs with Durham Habitat for Humanity partner families. And each of us, as voters and neighbors, can support initiatives that give families a fighting chance to own a piece of their hometown by donating today. Homeownership has always been the cornerstone of the American Dream – a source of stability, wealth-building, and pride. If we dismantle the systemic hurdles, we can open that dream to thousands more Durham families. It won’t be easy, but it is achievable. I believe in our community’s ability to innovate and invest in solutions. A Durham where every hard-working family can own a decent home is within our reach – and working together, we will make it a reality.

In the next part of this series, I will examine whether changing zoning rules – the “where and what we build” of housing – can help solve this affordability puzzle. Stay tuned.